Egg roll snack market trends are the demand and production shifts reshaping the category in 2026, led by air-fryer-ready formats, clean-label reformulation, cross-cultural flavor fusion, and record-high private label share. Beyond that headline, 2026 egg roll snack market trends will find at least three concurrent consumer shifts underway — air-fryer-ready format, clean-label reformulation, and cross-cultural flavor fusion — and precious little of the commentary will touch upon what any of that means for people working at the production line. WiseGuy Reports projects the global egg roll market growing from about $2.15 billion in 2025 to $3.2 billion in 2035 at a 4.0% CAGR, while the overall snack sector is growing at 4.2% CAGR according to Mordor Intelligence. Updated July 2026.

Quick Specs

| Global egg roll market (2025→2035) | $2.15B → $3.2B, 4.0% CAGR |

| US egg roll segment (2024) | $338.8M, 3.8% CAGR to 2031 |

| Frozen food processing machinery market (2025) | $21.1B, 4.5% CAGR 2026-2035 |

| Private label US grocery share (H1 2025) | 21.2% dollar / 23.2% unit, all-time high |

| Top 3 named trends | Air-fryer formats, clean-label/allergen-friendly, ethnic flavor fusion |

What’s Driving Growth in the Egg Roll & Crispy Roll Snack Category?

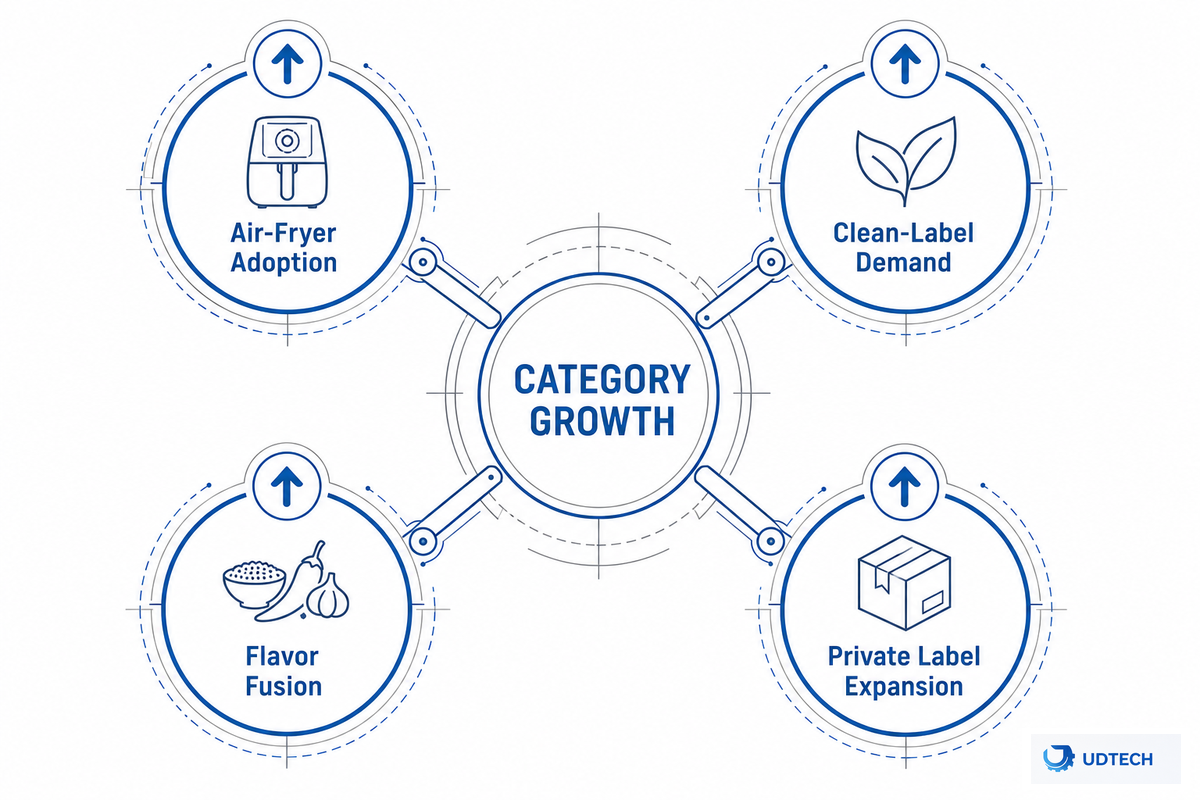

Egg roll and crispy roll snack market growth in 2026 is being driven by three converging forces rather than one single breakout trend: rising air-fryer-format adoption reshaping wrapper specs, clean-label and allergen-friendly reformulation pressure on batter and filling systems, and cross-cultural flavor fusion expanding filling variety, layered on top of steady underlying category demand.

Market size figures for egg roll snacks vary by tens of billions of dollars, depending on the scope of their analyses, and that range is one of the first things worth unpacking before one reacts to any of them. WiseGuy Reports estimates the global egg roll market will reach $2.15 billion in 2025, up from $3.2 billion in 2035 (4.0% CAGR), while Metastat Insight only estimates the 2024 US sales volume for the egg roll snack at $338.8 million, with 3.8% CAGR through 2031, roughly an order of magnitude lower because the global market is excluded from the calculation.

Neither vendor provides full details of its sampling methodologies, so take these figures with a grain of salt – they’re report-vendor estimates of global demand rather than an audited sum. And both are in part attributed to genuine snacking demand, in part to shifts in private label market share rather than solely a singular driving trend, and in both reports the market is expected to keep growing off that mixed base rather than off one clean driver. Independent market research reports on the underlying frozen and foodservice egg roll segment corroborate the overall market growth trajectory, if not the specific estimates — this market overview is a starting point for market segmentation by channel, not the final word.

And the health and wellness trends we detail in the next three sections are why this expanding market keeps producing a steady stream of ready-to-eat egg roll products rather than settling into a mature, static category — part of the market opportunities this article covers. In practice, the egg roll market is experiencing this growth unevenly: the egg roll market exhibits sharp variance by sub-format, and overall the egg roll market is characterized more by steady underlying demand than by explosive growth. Buyers should treat this as a baseline fact: egg rolls are typically a stable menu and freezer-case fixture rather than a novelty item, and incorporating egg rolls into a broader wrapped-and-filled product line — alongside dessert egg rolls, chicken egg rolls, and the traditional pork version — is how most manufacturers approach the category rather than betting on one SKU alone.

Once it’s broken down by segment rather than looked at as a singular, aggregate statistic, the total market number is more easily actionable.

Frozen retail and foodservice aren’t drawn from the same consumer demand curves, and few snack market reports provide specific breakdowns of egg roll products by segment, even though those market conditions vary dramatically from the supermarket to restaurant supply channels. Vegetable egg rolls and traditional egg rolls still represent the lion’s share of packaged egg rolls at the retail level; demand for egg rolls has held up through several years of consumer price sensitivity, with consumption of egg rolls holding steadier than many other discretionary snack categories even as consumers of egg rolls shift toward value-tier and private-label options rather than cutting the format out. Breaking the market into these components makes it a much more reliable snapshot of the opportunity landscape than looking at a single aggregate cagr – and it’s the frozen egg roll segment in particular where much of the market opportunities covered in the subsequent sections concentrate.

Better backdrop comes from category level scanner data. A Penn State Extension food trend review of 2026 using Food Institute scanner data notes that snacking occasions are up 17% y-o-y, and savory snack dollar sales were up in almost all reported segments in 2025 with rice cakes up ~25% and meat snacks up 13.1%. That’s a real, sourced signal that the overall wrapped-and-filled snack category is growing – even where egg-roll specific figures are slim.

A useful assumption to challenge upfront: a bigger market size doesn’t necessarily translate into more new equipment purchases. Research in this area, sometimes referred to as the “big market delusion”, suggests that many headline figures in market size for something like market growth reflect increased prices or market share shifts between incumbent producers, rather than expanded production capacity. Who’s winning that volume – whether in the broader snack food industry, or more narrowly in the egg roll and crispy roll sub-segment – dictates whether that growth actually impacts equipment procurement and will be explored later in this article. It’s critical to ask how market size is calculated. If you’re trying to compare different types of machines prior to sizing out a line, use the egg roll machine types and capacity guide in preference to a market size report.

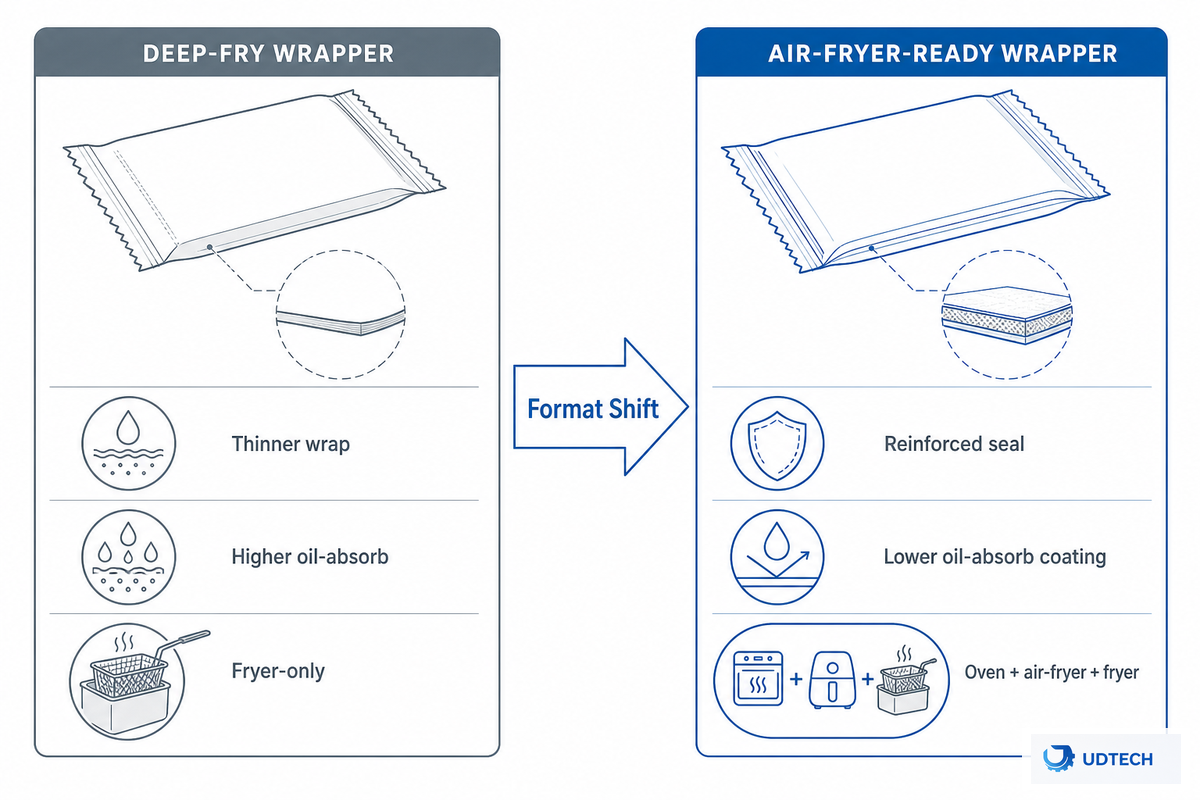

Trend 1, Air-Fryer-Ready Formats Are Rewriting Wrapper and Bake Specs

Air fryer readiness is an air fryer wrapper requirement that goes beyond a marketing claim. Today’s consumers expect crispy and browned products out of a countertop appliance rather than a deep fryer, requiring wrapper formulations that perform differently (lower moisture content, altered starch structures, better oil absorption) from fried products. A recent Packaging Corporation of America frozen foods bulletin highlighted that “right-sized, portioned packaging with strong moisture-resistant coatings are becoming common for reformed frozen snacks.” This is packaging equivalent of reformulating on the product side; the same reformulation logic sits under FDA’s FSMA traceability rule, which increasingly shapes how reformulated frozen SKUs get documented through the supply chain.

Unfortunately, we don’t have a lot of air fryer performance data specific to egg-roll wrappers. Available thickness and oil absorption data relates to neighboring fried snack matrixes, not specifically egg rolls, so the principles below are reformulations based on broader food science that are generally applied directionally. Skipping that test carries a real risk: a wrapper that isn’t reformulated cracks or turns rubbery in a countertop air fryer, and that failure mode shows up in customer reviews faster than almost any other product defect. In practice, you’d test a range of wrapper thickness (0.15-0.3mm is a common range for bake-not-fry applications) and look for a specific finished moisture level before committing a production run to bake-not-fry equipment rather than assuming frying performance will carry over. UDTECH’s engineering team runs this kind of wrapper-thickness trial in-house before recommending a spec change to a customer, because the mistake is expensive to discover after a production run is already committed.

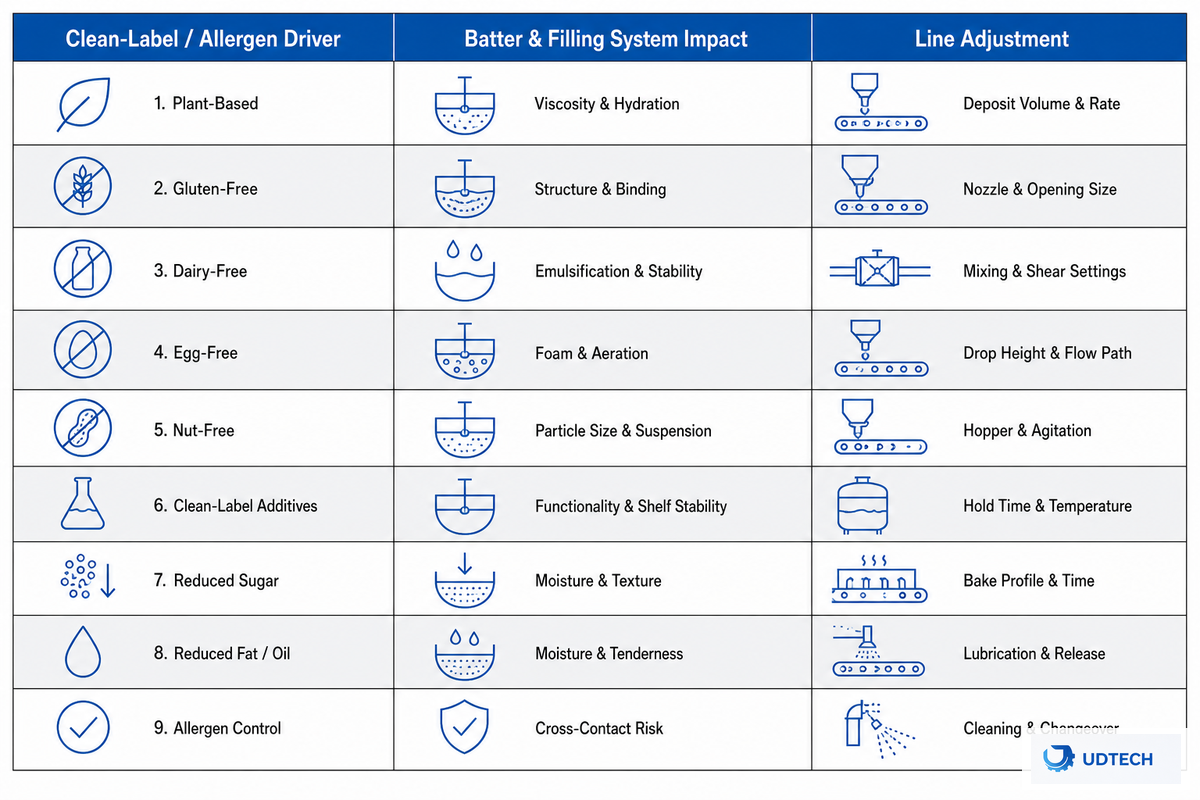

Trend 2, Clean-Label and Allergen-Friendly Demand Is Changing Batter & Filling Systems

A major factor in the definition of “healthy” among today’s consumers is what’s NOT there, and that change can be measured. According to a 2025 survey of food consumers by the International Food Information Council, mentioned by Penn State Extension’s 2026 food trends review, the percentage of consumers defining a healthy food as having “minimal or no processing” grew from 20% to 28% between 2022 and 2025. And “limited or no artificial ingredients” went from 18% to 25% over that period.

For an ingredient-shifting snack wrapped-and-filled concept, that can mean demand for gluten-free wrappers, organic vegetables fillings and protein-fortified options – all demanding a batter and filling system able to be retooled with little friction.

Allergen-friendly isn’t just a formulation adjustment. The Food and Drug Administration’s current Good Manufacturing Practice and preventive-controls rule makes food makers responsible for controlling cross-contact with allergens on their lines, and for verifying the accuracy of labels-meaning that any gluten-free or allergen-reduced SKU likely demands dedicated cleaning procedures, line segregation or scheduling controls on top of a formulation switch. Chalking up clean-label demand to merely a batter-recipe concern underestimates the true implications for operations on the floor. The 9-Row Trend-to-Line Translation Framework below maps every trend covered in this article to its production-floor consequence.

| Trend type / category | Production/spec implication | Adoption urgency |

|---|---|---|

| Air-fryer-ready formats | Wrapper moisture/thickness retuned for bake-not-fry; oil-uptake retest | Act now — active retail SKU shift |

| Gluten-free / allergen-friendly wrappers | Ingredient-swap-compatible batter system + dedicated cleaning/segregation protocol (FDA preventive controls) | Act now |

| Protein-enriched fillings | Filling viscosity/injection recalibration for higher-protein mixes | Watch — monitor SKU-level demand |

| Korean / Thai / Latin flavor fusion | Fast filling-injection changeover across multiple recipe profiles | Act now |

| Nori/seaweed roll format | Nori-feed synchronization; cross-machine format compatibility check | Watch — niche but growing |

| Private label / co-pack demand | Faster changeover for multi-brand SKU runs; flexible packaging integration | Act now |

| Textural contrast (crispy/flaky/airy) | Multi-stage forming/baking to layer textures within one product | Watch |

| Portion/format shifts (single-serve, snack-size) | Format/size changeover on forming and cutting stations | Watch |

| Input-cost volatility (eggs, produce) | Recipe cost-modeling flexibility, not a line-hardware change | Background — monitor |

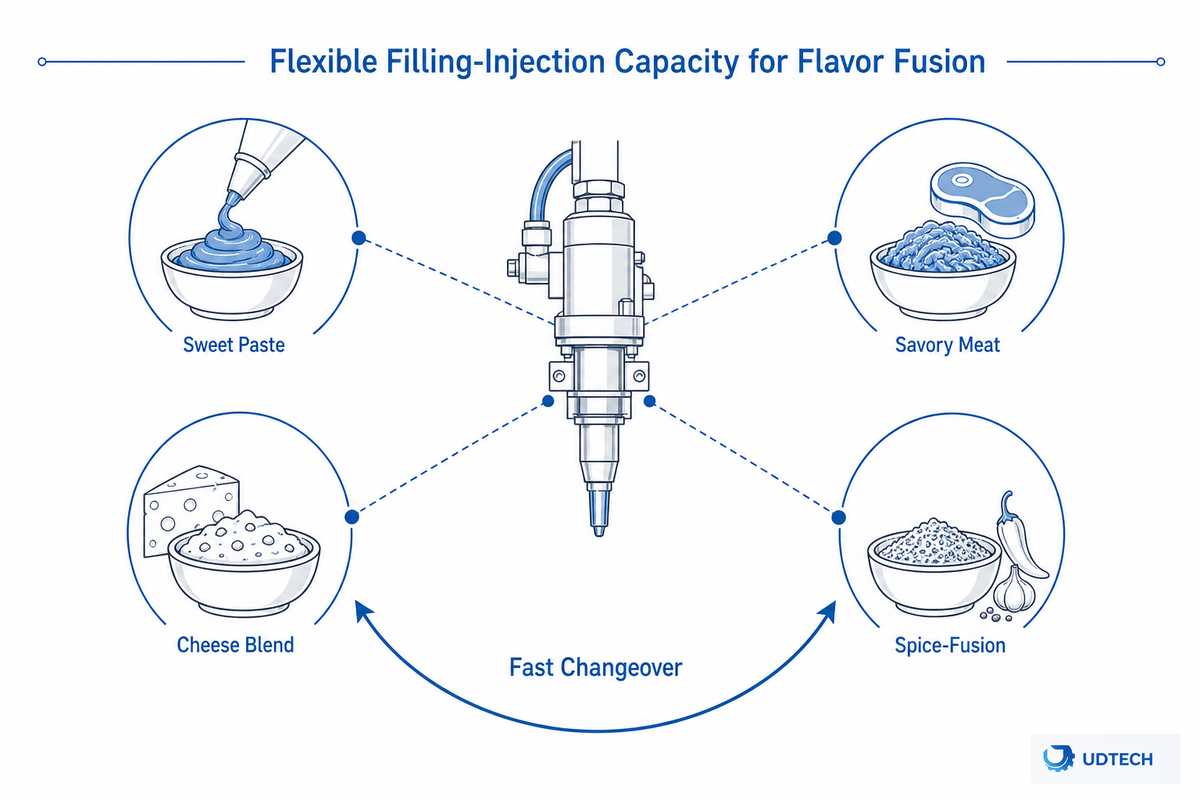

Trend 3, Ethnic Flavor Fusion Needs Flexible Filling-Injection Capacity

Cabbage-and-pork may be traditional for egg roll and crispy roll, but that’s no longer the whole narrative. By 2026, flavor development is coalescing around named flavor combinations, according to Supermarket Perimeter and Refrigerated & Frozen Foods, as quoted by Penn State Extension’s 2026 food trends review: “swokey” (sweet + smoky, i.e. BBQ and chipotle); “swalty” (sweet + salty, i.e. salted honey and miso caramel); “swangy” (sweet + spicy + tangy); and “savery” (sweet + savory, i.e. teriyaki and miso brown butter).

For the snack manufacturer, that naming is a filling recipe map. A Korean barbecue, a Thai chili-lime and a Latin-influenced filling are simply all iterations on the already-successful “swicy” / “swokey” in neighboring snack product categories. Updated egg roll recipes built around these flavor pairings are showing up first in foodservice, where freshly prepared egg rolls that cater to a specific local audience can test a flavor before it commits to a frozen SKU.

And what that translates to on a production line is changeover speed, rather than new hardware in many cases. A filling/injection machine that can go from three or four recipe profiles in a single shift captures this trend better than a machine dedicated to one filling – and because none of the flavor-fusion coverage in this article even discusses hardware, this is the information translation that this part is here to provide.

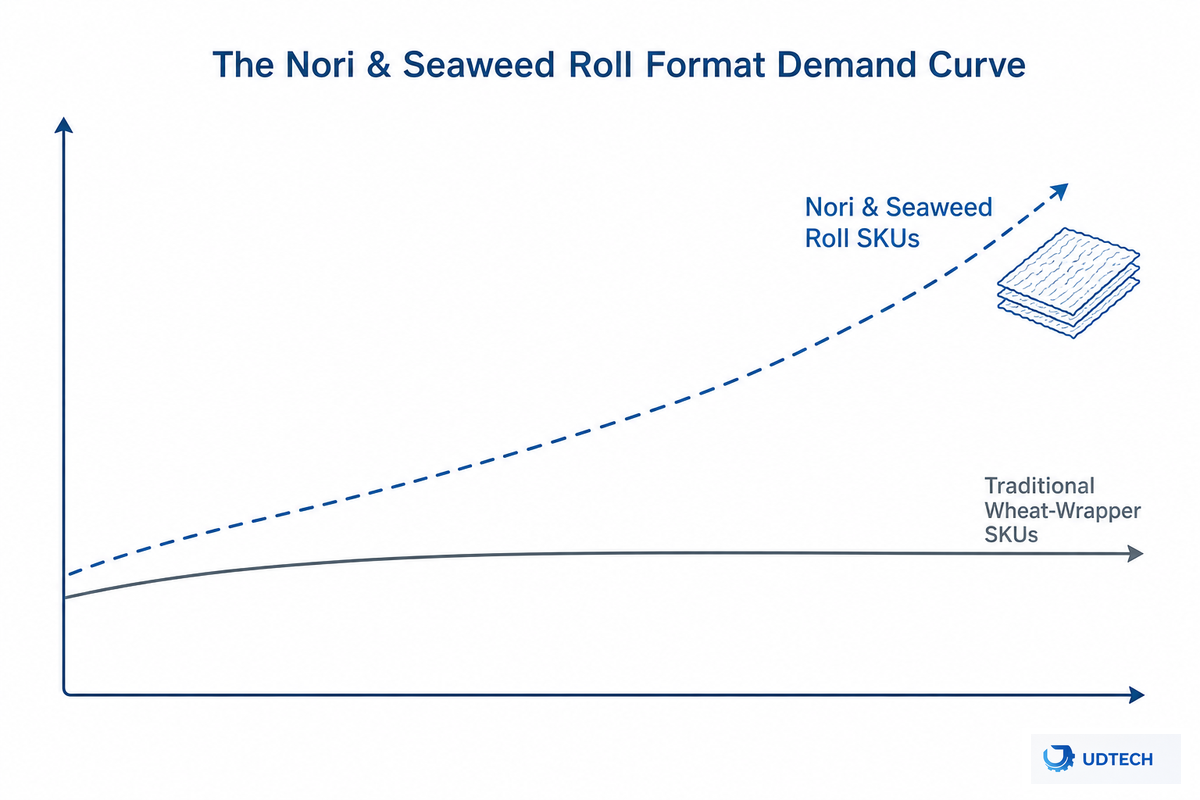

The Nori & Seaweed Roll Format Is Carving Out Its Own Demand Curve

The seaweed-wrapped roll format sits in a smaller, more specialized niche than the primary egg roll market, and it’s different enough to warrant treating as a distinct planning issue rather than lumping it into the total market-sizing discussion above. One useful data point if you’re formulating: government nutrient composition data lists dried nori at about 116 micrograms of iodine per 5-gram serving — roughly 77% of the daily recommended value. Iodine content will of course differ depending on the specific seaweed species and where and how it’s harvested and processed. Treating a nori-format line as a simple wrapper swap on existing equipment is a common mistake; the risk is torn or unevenly hydrated nori sheets, which is a distinct challenge from the dough-based wrapper problems covered above. UDTECH’s engineering team has fielded this exact question from customers evaluating a seaweed line for the first time, and the answer is almost always a nori-feed synchronization test before committing capital.

For a UDTECH reader considering whether this format warrants a production line: the planning question is nori-feed synchronization and cross-machine format compatibility, not forecasting demand – that’s covered from the consumer demand angle in What Is a Seaweed Egg Roll and from the machine-selection angle in the seaweed egg roll machine buying guide — this section stays narrow to avoid repeating either.

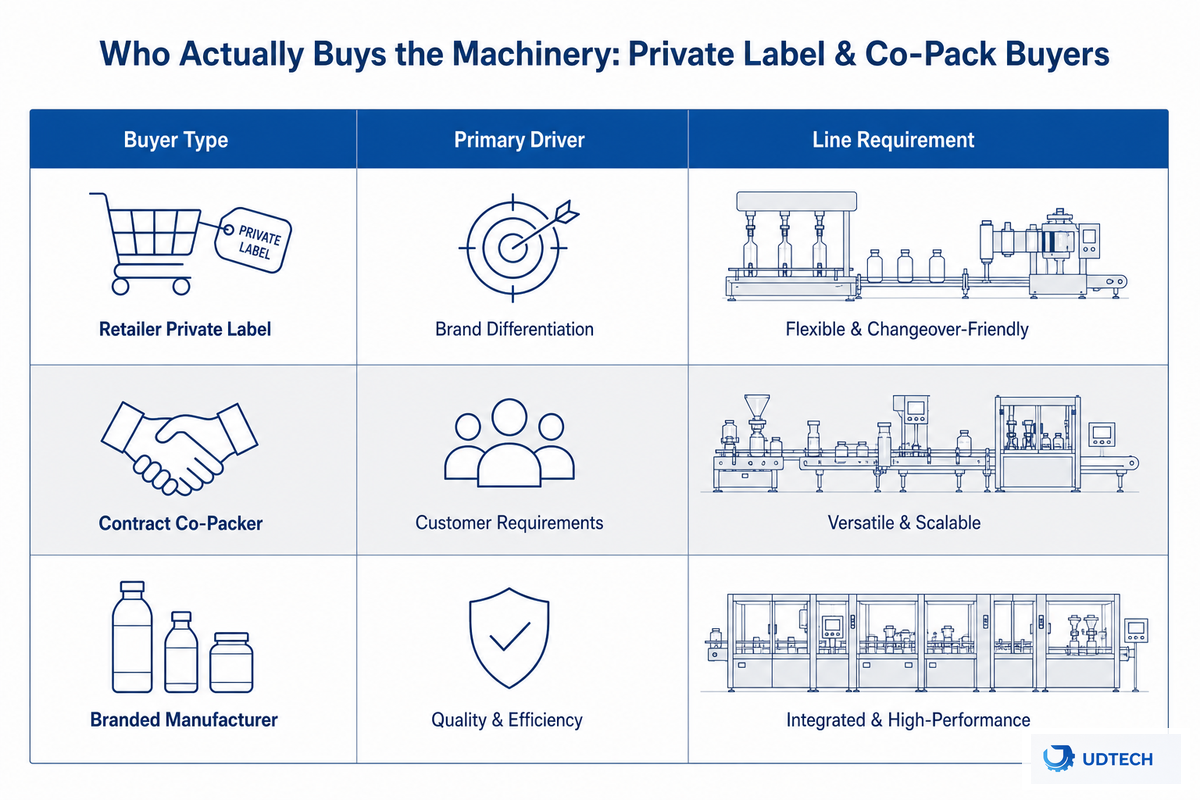

Private Label and Co-Packing Are Reshaping Who Actually Buys the Machinery

Store-brand snacks have moved from budget after-thought to a category leader, with retail data clearly validating the claim. US private label dollar sales increased 4.4% in the six months ending June 15 versus the year before, according to Just Food citing Private Label Manufacturers Association (PLMA) data, while national brand dollar sales increased by just 1.1% and national brand unit sales actually decreased by 0.6%. PLMA shows Private label’s dollar market share is a record high 21.2% dollar sales share, while its unit share is 23.2% and the group is forecasting the PLMA market value to grow to approximately $277 billion in 2025 from $271 billion in 2024 – third straight year the private label share of sales grew both in dollars and in units versus national brands.

That retail data doesn’t explicitly indicate who’s buying the equipment on the back end for these shelves. A retail share number tells you who purchased from a shelf, not who purchased the line to fill that shelf; that role could be fulfilled by the brand owner, the co-packer of that brand, and even a retailer-affiliated processor. Inferring a wholesale shift in buyer profile from the PLMA share data is reasonable as a trend indicator, but it’s not an investment-level dataset, so keep it in mind without overweighting it.

| Buyer profile | What they’re optimizing for | Equipment implication |

|---|---|---|

| Branded snack maker | Flavor differentiation, brand equity, premiumization | Flexible filling-injection for frequent new-flavor launches |

| Private-label / co-pack operator | Fast changeover, margin protection (private-label margins can exceed 40% vs. 25-35% for national brands, per Just Food’s margin analysis) | Multi-SKU changeover speed, format flexibility across retailer specs |

| Foodservice distributor | Consistent bulk output, portion-control accuracy | Throughput consistency over recipe variety |

Data Boundary: Buyer Profile Mapping is a reasonable inference from retail share data, and from the industry’s market structure, not a direct capital expenditure survey.

“The brands — retailer or manufacturer — that win over the next five or so years will be those that keep one eye on margin and the other on meaning, delivering not just products but reasons for shoppers to believe. History is on the side of manufacturer brands but private-label brands are clearly catching up.”

— Victor Martino, Just Food

Splitting the egg roll market by product type shows this shift clearly: gourmet egg roll positioning at premium retailers sits alongside value-tier private label, and the economics of making egg rolls at co-pack scale increasingly favor whichever operator can run both tiers on the same line. Roughly 90% of Aldi and Trader Joe’s SKUs are store-brand, and Kirkland alone represents 31-33% of the sales at Costco – volumes that are now likely supported by production that’s too much of an in-line investment for a national brand’s overfill and so has to be dedicated to the PL account. This isn’t unique to egg rolls: private label chips and other snack food manufacturers are riding the same crispy snack shift, and the broader snack industry trends behind this snack market growth — including the healthy snack trend covered above — extend well past this one format. The phoenix roll and wafer categories wouldn’t be discussed herein if there were no overlaps in opportunity space between that category of SKU and the egg rolls- that’s the reason we refer the reader to the phoenix roll snack overview in a previous UDTECH post.

Regional & Channel Shifts Worth Tracking

North America will be estimated to make up around 31.3% of the private-label food packaging market by 2026, outranking Asia Pacific’s estimated share of 24.5%, per an egg roll market research report from Coherent Market Insights (a market research firm whose data should be read directionally rather than as gospel) — one of several egg roll market regional breakdowns worth cross-checking before committing to a single geography; for US manufacturers the market in North America still remains primary in terms of size planning for that sector of product, even though the PL category’s flavor inspirations have become globalized; but within the sector the regional mix of the customer base should be considered alongside the Channel mix-where in foodservice, volume and speed throughput are paramount, but at retail and for PL, turn over rate is what most counts-two market dynamics that a national market share statistic can gloss over in one broad brushstroke — evaluating each market segment on its own terms, rather than assuming uniform market expansion across the category, is the more disciplined read. Getting this wrong carries a costly risk: a line sized for foodservice throughput can sit underutilized if the real growth is happening in the private-label retail channel, or vice versa — a mistake UDTECH’s engineering team sees often enough among first-time buyers that it’s worth naming directly.

There’s a real gap between when a trend appears in retail, and when it’s translated into new production capacity-call it the consumer-to-conveyor lag. Federal Reserve Bank of Chicago research has identified two principal reasons manufacturers are slow to invest in new equipment, even after the trend hits shelves-not their lack of awareness-credit constraints and uncertainty over the eventual usefulness of a new technology. No dataset measures the consumer-to-conveyor lag in terms of snack production years, but consider this a mechanism to observe rather than a timeline; the manufacturer that can get these funding and technology questions resolved early in the process has an edge at grabbing shelf space. Line configuration will also affect how fast you can capitalize on the trend — see the continuous vs. batch production comparison for details on output format.

What These Trends Mean for Your Production Line Roadmap

Turning 2026’s egg roll and crispy roll trends into a production line roadmap starts with triage, not a blanket retool: act now on air-fryer wrapper retuning, FDA-mandated allergen segregation, and multi-flavor filling-injection flexibility, while watching nori/seaweed capacity and textural-contrast forming until demand is confirmed.

Not every trend in this article merits an immediate capital investment, and treating them all in the same fashion would be an error in itself. Running an Act-Now vs Watch-and-Wait Trend Triage — ordering these trends by their likely impact on equipment procurement rather than their visibility in the media — is a more reasonable approach than simply reacting to whatever has recently captured industry headlines. Interest in egg rolls as a category is hardly new — the market for egg rolls has grown at retail for years with little investment in new production capacity — and the gap that this trend triage seeks to close is precisely the gap between the popularity of egg rolls at retail and low awareness of egg roll production challenges.

- Air-fryer wrapper/spec retuning — active SKU shift already underway at retail

- Allergen-friendly line segregation — required by FDA preventive controls, not optional

- Multi-flavor filling-injection flexibility — captures both flavor fusion and private-label changeover demand

- Nori/seaweed dedicated capacity — real but still a niche format, confirm demand before committing a line

- Textural-contrast multi-stage forming — emerging, worth monitoring before a full retool

- Input-cost-driven recipe changes — model cost impact, don’t rebuild hardware around it

The wafer egg roll line from UDTECH embodies the quick-changeover production that the roadmap describes; the UDTECH line has the rapid filling profile switching and format versatility necessary to accommodate the varied output that will come from an adaptation of the wafer egg roll line in the future-whether this includes adapting the filling system for savory or seaweed products, or developing allergen-friendly and clean label variants. For those seeking to design or assess new equipment capacity according to the roadmap’s projections, the procurement guide for UDTECH’s wafer egg roll line covers price ranges, lead times and installation requirements, while the capacity planning breakdown will help you size a line against actual market demand, not market growth projections.

Market-size headlines ($2.15B-$3.2B by 2035) don’t predict equipment demand as reliably as private label’s 21.2% share shift and FDA-driven allergen-control requirements do — plan capacity around buyer behavior, not CAGR.

Frequently Asked Questions

Q: Are egg rolls popular?

Yes — egg rolls remain one of the most consistently ordered items in American Chinese cuisine and have grown into a stable, multi-hundred-million-dollar retail and foodservice category.

Q: What are the biggest food trends right now?

For the egg roll and crispy roll category specifically, the three biggest shifts are air-fryer-ready formats, clean-label and allergen-friendly variants, and cross-cultural flavor fusion — each with a direct production-line implication.

Q: What snacks are in high demand?

Wrapped-and-filled formats — egg rolls, spring rolls, wontons, and the growing nori/seaweed roll segment — are in high demand alongside protein-forward reformulations, with private-label versions capturing a growing share of that demand.

Q: Which product type dominates the egg roll market?

Traditional cabbage-and-pork or cabbage-and-vegetable frozen egg rolls remain the dominant product type by volume across both retail and foodservice channels, though flavor-fusion and clean-label variants are the fastest-growing sub-segments and are where most of the new production investment is concentrated.

Q: How can businesses capitalize on the growth of the egg roll market?

Prioritize production-line flexibility — fast filling-injection changeover and allergen-segregation capability — over chasing the highest market-size headline number, and size capacity to your own channel mix rather than to one aggregate growth figure.

Q: What are the key factors driving growth in the egg roll market?

Three factors: broader snack-sector expansion (4.2% CAGR), private label’s structural share gains (21.2% dollar share, an all-time high), and consumer demand for healthier, globally-inspired flavor reformulations.

Related Articles

- Egg Roll Machine: Types, Capacity & Buyer’s Guide — compare machine types before sizing a line

- Egg Roll Machine Capacity Planning — size a line against real demand, not headline market growth

- What Are Chinese Egg Roll Cookies? — the wafer-cookie side of the category

- What Is a Phoenix Roll? — the seaweed and pork floss adjacent snack category

References & Sources

- Food Price Outlook, Summary Findings — USDA Economic Research Service

- Food Trends 2026 — Penn State Extension

- Food Allergies — U.S. Food and Drug Administration

- Iodine, Health Professional Fact Sheet — National Institutes of Health, Office of Dietary Supplements

- How Do Manufacturers Decide When to Invest in New Equipment? — Federal Reserve Bank of Chicago

- Private Label’s Growth Surge and the US Brand Battle Ahead — Just Food

- The Big Market Delusion: Valuation and Investment Implications — Financial Analysts Journal

- Egg Roll Market Analysis & Growth Projections — WiseGuy Reports (report-vendor estimate, directional)

- US Egg Roll Market Size, Share, Trend — Metastat Insight (report-vendor estimate, directional)

Our Perspective

UDTECH builds the wafer egg roll production lines that manufacturers are already using to respond to the very trends outlined in this article – air fryer wrappers, allergen segregating batters and rapid-fill injection systems. We published this piece because most market coverage of egg rolls begins and ends with the headline growth figure and fails to address what it means for production equipment, which is the core expertise that we spend our time sharing with our customers. Reviewed by Suzhou UDTECH Technology Co., Ltd. technical team.